Meal Vouchers - Legal Requirements

There are new legal requirements starting 2023 for using digital meal vouchers.

Expense Management

Expense Management Employee Benefits

Employee BenefitsThere are new legal requirements starting 2023 for using digital meal vouchers.

Sophie Jordan

Sophie JordanThe decision made on August 20, 1997 (BStBl. II p. 667) by the BFH dictates that employers and employees can replace cash wages with benefits by mutual agreement. Since then, corporate benefits have become a popular method in Germany to meet the needs of employees and present the company as a valuable employer. If the applicable limits for non-cash benefits are met, zero or only low taxes and social security contributions are to be paid because of the benefits. So they don't just promote employee motivation, employers can also save money, as a salary increase, through corporate benefits is more favorable than an ordinary salary increase.

Since February 2, 2016 digital meal vouchers have also been possible in addition to physical meal vouchers (BStBl 2016 I p. 238). Digital meal vouchers have the clear advantage since they can be used anywhere; at the supermarket, restaurant, delivery service or the bakery around the corner. Especially when working from home, this is a benefit that companies can make available to their employees without restrictions.

This article provides an overview of the currently valid legal requirements of meal vouchers.

The meal allowance is made up of two parts, a tax-free part and a taxable part. The non-cash benefit value for lunch has been €3.80 since January 1, 2022. The valid, official non-cash benefit value for meals is determined by the BMAS, based on the development of consumer prices in the previous year, and thus changing annually.

This non-cash remuneration value forms the basis of the meal allowance and is taxable for the employer at a fixed rate of 25%. In addition, the employer can provide up to €3.10 tax-free. Thus, the maximum allowance per day is €6.90 (2023).

On January 18, 2019, the BMF published a letter entitled: Sachbezugswert für arbeitstägliche Zuschüsse zu Mahlzeiten (non-cash benefit value for workday meal allowances). This letter provides the legal basis for (digital) meal vouchers, replacing the BMF document dated February 24, 2016 (BStBl I page 238). It is to be applied in all open cases.

Recognition of the applicable official non-cash benefit remuneration value

If the employer's benefits consist of employee entitlement to daily allowances for meals agreed upon in the employment contract or according to other legal basis under employment law, the employee's meal, rather than the allowance, is to be recognized as remuneration for work at the applicable official value of remuneration, pursuant to Sozialversicherungsentgeltverordnung (SvEV), if it is ensured that:

This applies even if there is no contractual relationship between the employer and a company such as a restaurant, bakery or delivery service that provides the subsidized meal. There is also a limit of a maximum of 15 meal subsidies in a calendar month.

The employer is obliged to either manually check the itemized receipts submitted by the employee, or to make use of corresponding electronic procedures, such as when a provider digitizes the receipts completely & automatically, checks them and forwards a monthly statement to the employer, from which the same findings can be obtained as from the itemized receipts. The employer must retain the receipts or the payroll account statement.

Workday meal allowances are to be recognized at the applicable official non-cash remuneration value, even if they are paid to employees who either work from home or don't work more than six hours a day, even if the company's working time regulations do not provide corresponding breaks.

Allowances for meals on working days are to be recognized at the applicable official non-cash remuneration value even if the employee purchases individual components of his meal at several different location.

For every working day and each subsidized meal (breakfast, lunch or dinner), only one subsidy may be recognized at the official non-cash benefit value. If the employee purchases additional meals for other days on the same day, the subsidies granted for these meals must be recorded as cash wages. The same applies to the individual purchase of components of a meal in stock.

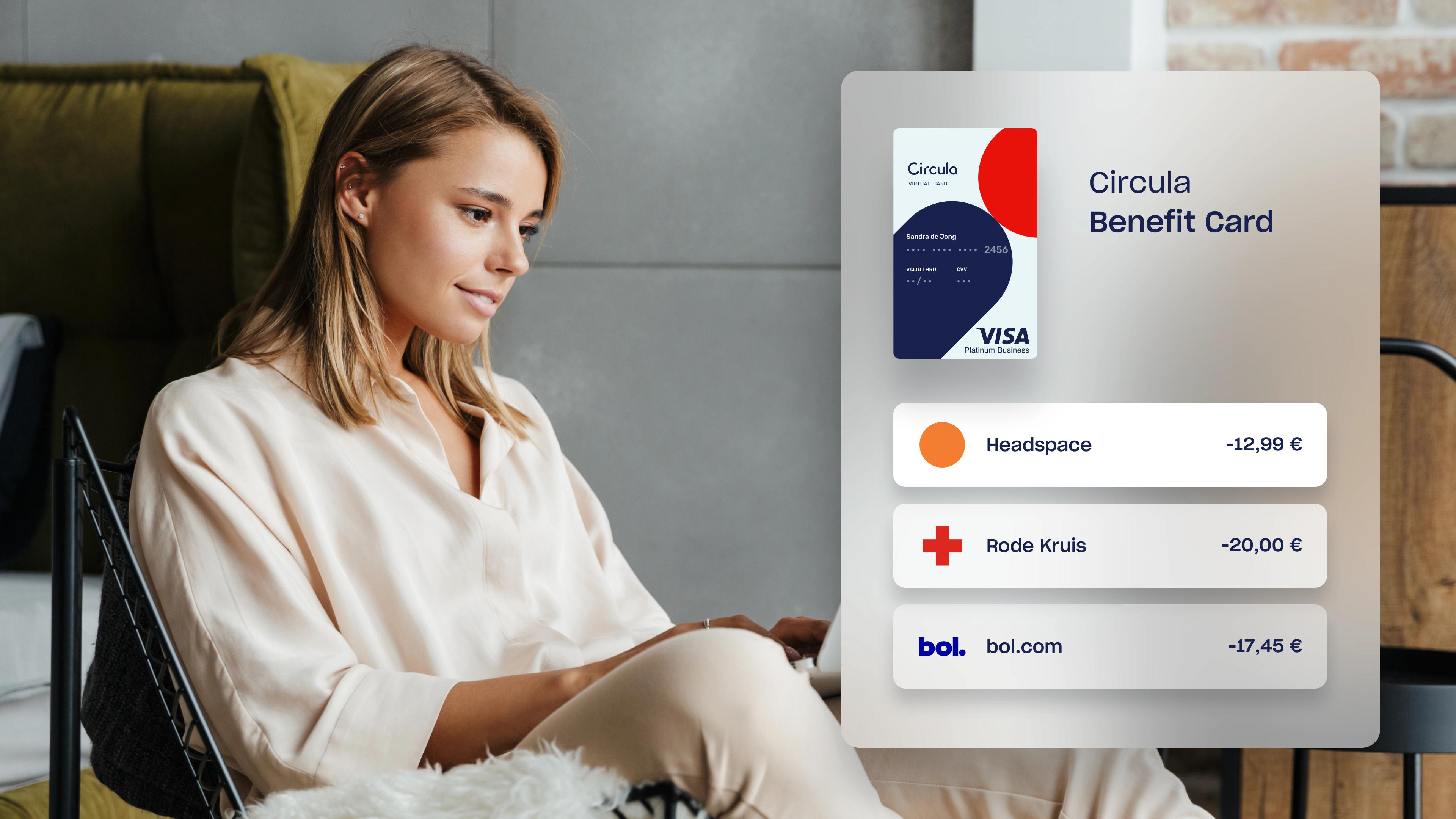

Would you also like to get these tax benefits?

With Circula Benefits you can strengthen employee loyalty and satisfaction, and additionally create legal compliance within your company. Contact us, we're more than happy to look at the best options for you!

Circula is the ideal partner for your expense management. Circula's makes it easy to account for all employee expenses - per diems, cash expenses, travel expenses, and out-of-pocket expenses. The intelligent Circula adapts perfectly to your business processes and offers further premium benefits with attractive cashbacks. In addition, Circula offers companies tax-optimized such as the , a flexible and with which employees can be supported.

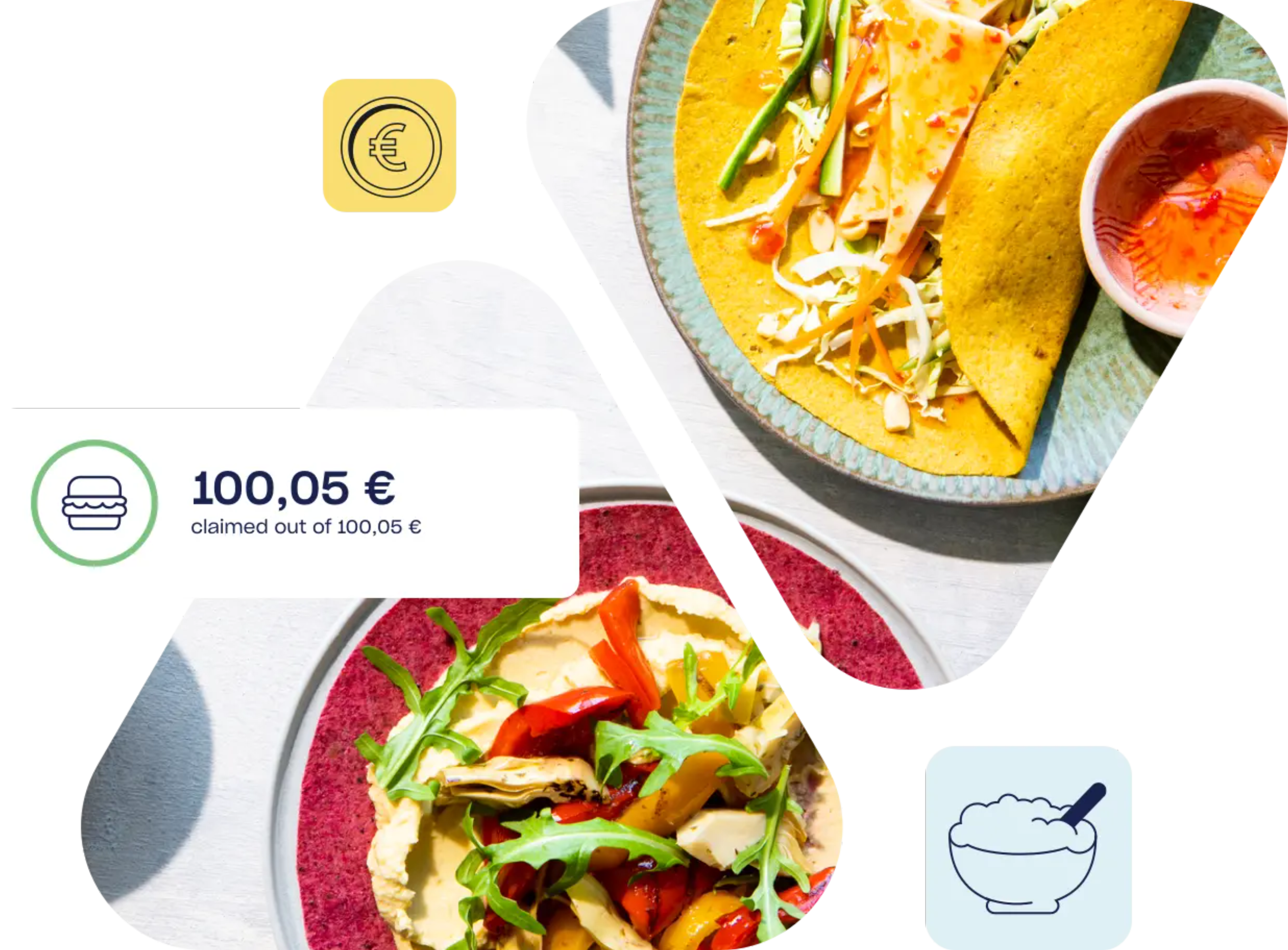

Provide lunch for your employees and show your appreciation, increasing employee engagement and talent retention for your company.

Book a demo